Real Estate Wire Fraud: The $275 Million Problem Hitting Closings in 2026

The FBI’s newest numbers say real estate fraud losses grew 58 percent in a single year. If you run a brokerage, a title office, or a real estate law practice, the scam is aimed at your inbox, and increasingly, the lawsuit is aimed at you.

Real estate wire fraud is a scam in which criminals compromise or impersonate the email of a party to a real estate transaction, usually a title company, agent, or attorney, and send fraudulent wire instructions timed to closing, diverting the buyer’s funds to an account the criminals control.

Key Takeaways

- The FBI's Internet Crime Complaint Center (IC3) logged 12,368 real estate fraud complaints in 2025 with $275.1 million in losses, up from $173.6 million in 2024.

- Business email compromise, the mechanism behind most closing scams, was the second-largest cybercrime loss category at $3.04 billion.

- No rule automatically assigns the loss to the buyer. Courts look at which professional failed to exercise reasonable care, and agents, brokers, title companies, and law firms have all been named.

- A documented call-back verification protocol on every wire is the single cheapest control a real estate business can run.

- Speed decides recovery: the FBI's Recovery Asset Team froze $679 million of $1.16 billion in attempted thefts in 2025, a 58 percent success rate, but only when victims reported fast.

If you work in residential real estate, you already know the story shape: a buyer gets an email that looks exactly like it came from the title company, wires their closing funds, and shows up to a closing table where nobody has the money. What changed in 2025 is the scale, and who ends up paying.

What the FBI’s 2025 Numbers Actually Say

The FBI IC3 2025 Internet Crime Report, released in April 2026, is the primary source for how bad this has become.

The headline figures:

| Metric | 2025 | 2024 |

|---|---|---|

| Real estate fraud complaints | 12,368 | 9,359 |

| Real estate fraud losses | $275.1M | $173.6M |

| BEC losses (all industries) | $3.04B | n/a |

| Total IC3 losses | $20.877B | +26% YoY |

Two details in the report matter more than the totals.

First, the mechanism. Business email compromise ranked second among all loss categories at $3.04 billion across 24,768 complaints, and real estate closings are one of its favorite targets: a large, one-time, irreversible transfer, on a publicly discoverable timeline, coordinated over email between parties who have often never met.

Second, the AI acceleration. IC3 received more than 22,000 complaints referencing AI in 2025, with adjusted losses above $893 million. The report specifically flags chat generators producing convincing impersonation emails and voice cloning used to request wire payments. The sloppy, typo-ridden scam email is dying. What replaces it reads like your escrow officer on a normal Tuesday. We covered how unmanaged AI tools create this kind of exposure for small firms in our shadow AI breakdown.

How the Scam Works at a Closing

The pattern documented across IC3 case examples is consistent:

- Compromise. Criminals phish or credential-stuff their way into the mailbox of one party, most often an agent or a title/escrow employee. Sometimes they never breach anyone and simply register a lookalike domain.

- Surveillance. They read quietly, sometimes for weeks. They learn the property address, the closing date, the parties, the tone everyone uses.

- The strike. Days or hours before closing, the buyer receives wire instructions, or a “correction” to instructions already sent, from what appears to be the title company or attorney. The branding, signature block, and thread history all look right.

- The wire. The buyer sends the funds. By the time anyone notices, the money has been forwarded through mule accounts, frequently converted to cryptocurrency.

One IC3 case from 2025: a senior in Missouri closing on a property received an email from a spoofed “title company” with wire instructions for over $1.3 million. Another couple wired more than $449,000 after receiving an email impersonating their own attorneys. In both cases the FBI’s Financial Fraud Kill Chain froze the funds, but only because the fraud was reported quickly. Most victims are not that fast, and most money is not recovered.

Who Is Liable When Closing Funds Go to a Scammer?

This is the question that should keep brokerage owners and title office managers up at night, because the answer is not “the criminal.”

There is no statute that cleanly assigns the loss. In litigated cases, courts have apportioned responsibility among buyers, agents, brokers, title companies, and law firms by asking who owed a duty of care and who failed to exercise reasonable care in protecting the transaction. The American Bar Association’s published analysis of real estate wire fraud cases describes exactly this pattern: the criminal is untraceable, so the parties left standing sue each other.

In practice, the exposure for a real estate business looks like this:

- If your email account was the one compromised, expect to be a defendant. Failure to use MFA and basic email security reads as negligence to a jury.

- If your side sent instructions by unencrypted email with no verification step, expect that procedure to be exhibit A.

- If your disclosures never warned the client about wire fraud, the absence will be noticed. Warning language in engagement documents and email signatures is now standard in the industry precisely because of these suits.

The reputational half is worse. A brokerage whose client lost a down payment does not get that client back, and closing-scam stories travel fast in a local market.

How Scammers Know You’re Closing

Buyers ask this constantly, and the answer is unglamorous: mostly, they read it. A compromised agent or title mailbox exposes every pending transaction at once, which is why one breached employee inbox can seed a dozen frauds. Beyond that, listing data going pending, public records, and social media posts (“we close Friday!”) give criminals the timeline even without a breach. The lesson for a business is that you cannot keep the closing secret. You can only make the wire path verification-proof.

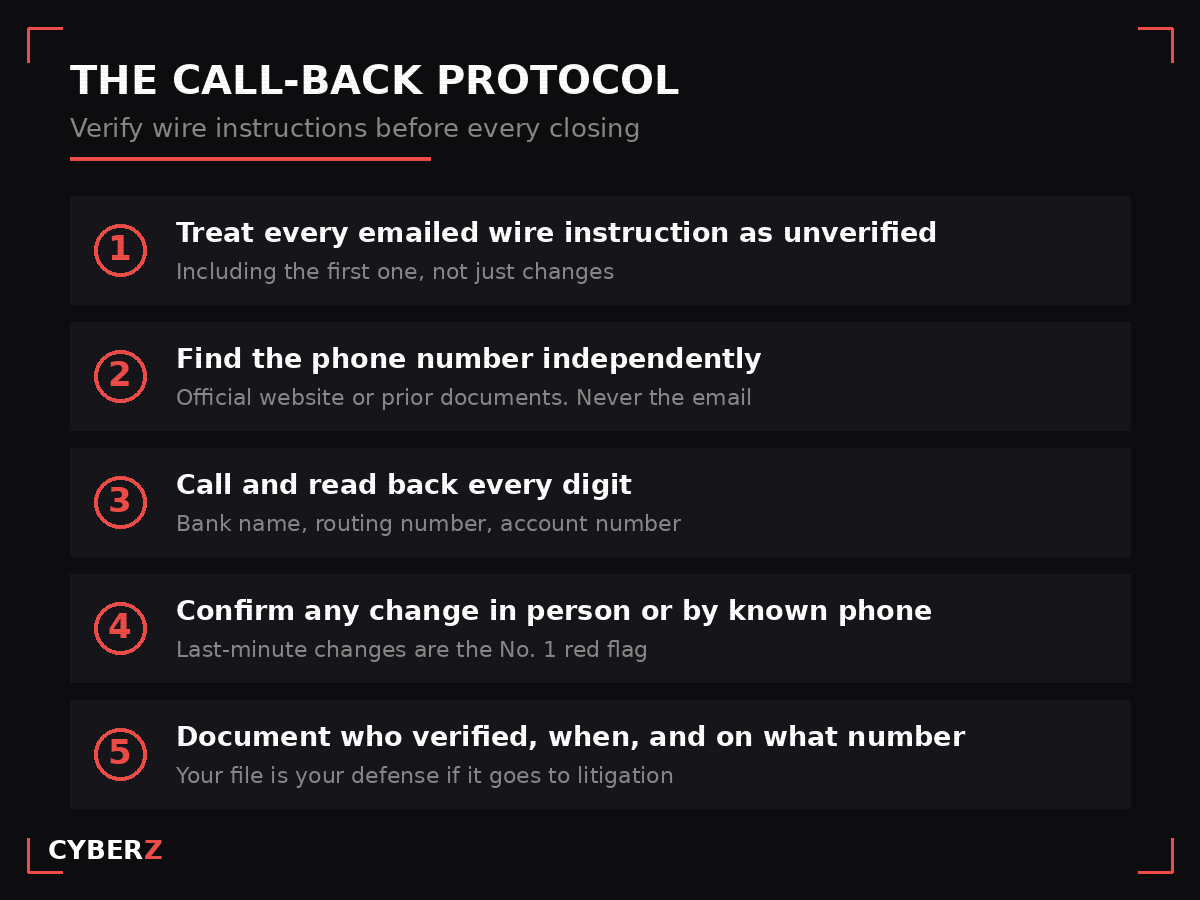

The Call-Back Protocol: Verifying Wire Instructions Before Closing

Every serious prevention framework, from the FBI to the Consumer Financial Protection Bureau’s mortgage closing scam guidance, converges on the same core control: independent verbal verification of wire instructions, every time.

The protocol that holds up:

- Treat every emailed wire instruction as unverified. Including the first set, not just changes.

- Find the phone number independently. From the title company’s official website or from documents exchanged at the start of the transaction. Never from the email containing the instructions, and never by replying to ask “is this real?”

- Call and read back every digit. Bank name, routing number, account number, beneficiary name.

- Treat any change to instructions as hostile until proven otherwise. A last-minute change to wiring instructions is the single most reliable red flag in the entire scam.

- Document the verification. Who called, what number, when, what was confirmed. If a fraud happens anyway, that record is the difference between “we followed a written procedure” and “we have no idea.”

For agents, the client-facing version of this belongs in your first buyer meeting, your engagement paperwork, and your email signature. The step-by-step client script and verification checklist is what Verifying Wire Instructions: Real Estate Fraud Defense ($35) packages for exactly this use.

If the Money Already Moved: The First 72 Hours

Recovery is a race. IC3’s Recovery Asset Team initiated 3,900 Financial Fraud Kill Chain actions in 2025 and froze $679 million of $1.16 billion in attempted thefts, a 58 percent success rate. That rate collapses with delay, because mule accounts drain in hours.

The sequence, the moment a fraudulent wire is discovered:

- Call the sending bank immediately. Request a wire recall and ask them to invoke a fraud freeze with the receiving bank.

- File at ic3.gov, same day. The IC3 complaint is what triggers the Financial Fraud Kill Chain. Include the recipient account details, amount, and date.

- Notify the receiving bank’s fraud department directly as well.

- File a police report and preserve every email, header included, untouched.

- Notify your insurer and counsel. Cyber and E&O policies have notice deadlines measured in days.

Every real estate office should have this taped up before it is needed. The hour-by-hour playbook, with contact scripts for banks and the IC3 filing walkthrough, is the job of Wire Fraud Response for Real Estate: Emergency Guide ($49).

Building a Prevention Program for a Brokerage or Title Office

Individual vigilance does not scale. A 20-agent brokerage or a 10-person title office needs the controls to be procedural, not heroic:

- MFA on every email account, no exceptions. Most of these frauds begin with one compromised mailbox.

- A written wire communication policy. Instructions delivered through a defined channel, changes forbidden by email, verification documented.

- Client warnings early and in writing. Engagement documents, email signatures, and a verbal warning at the first meeting.

- Team training with real scenarios. New hires are the soft target; the scam counts on someone who has not seen it before.

- An incident playbook (see the 72-hour sequence above) that everyone can find.

The starting point for a single closing workflow is Wire Fraud Prevention for Real Estate: Closing Guide ($49). If you are standardizing this across a whole team ahead of your busy season, or a carrier or client is asking to see your written procedures, the Wire Fraud Prevention Bundle for Real Estate Closings ($127) packages the closing guide, verification protocol, communication policy, team training, and emergency response in one set.

The Bottom Line

Real estate wire fraud grew 58 percent in a year because it works: one convincing email against one irreversible transfer, timed to the most distracted day of the transaction. The FBI’s own data shows the two levers that matter are verification before the wire and speed after it. Both are procedures, not products, and both are decided by what your office writes down before the scam email ever arrives. The businesses that lose are not the unlucky ones. They are the ones that treated wire security as the client’s problem.

Sources

- FBI Internet Crime Complaint Center, 2025 Internet Crime Report (ic3.gov)

- FBI IC3 Recovery Asset Team / Financial Fraud Kill Chain case data, 2025 Internet Crime Report

- Consumer Financial Protection Bureau, “Mortgage Closing Scams: How to protect yourself and your closing funds” (consumerfinance.gov)

- American Bar Association, “An Analysis of Real Estate Wire Fraud Cases” (americanbar.org)